In my opinion, expense accounts are essential tools for businesses to track and manage their spending effectively, providing valuable insights into financial health.

Expense accounts are detailed records meticulously maintained by businesses to systematically track and categorize their expenditures, encompassing a wide range of costs, from day-to-day operating expenses to significant capital investments.

In this article, we will explore the importance of expense accounts in financial management and delve into best practices for effective expense management.

What Is An Expense Account – Let’s Explore!

An expense account is a financial record used to track and categorize expenditures incurred by individuals or businesses in their day-to-day operations.

It serves as a detailed ledger where all expenses, ranging from overhead costs like rent and utilities to smaller purchases like office supplies, are documented.

By maintaining an expense account, individuals and businesses can gain insights into their spending habits, identify areas of excessive expenditure, and implement strategies to manage their finances more effectively.

Furthermore, expense accounts play a crucial role in financial management and reporting. They provide the necessary data for creating accurate financial statements, including income statements and balance sheets.

This information is essential for assessing profitability, evaluating financial health, and making informed decisions about resource allocation and investment.

Overall, expense accounts are indispensable tools for maintaining financial transparency, controlling costs, and achieving long-term financial stability.

Types Of Expense Accounts – Dive In It!

Operating Expenses:

Operating encompasses the day-to-day expenditures necessary for running a business efficiently. These expenses include costs like rent, utilities, salaries, office supplies, marketing, and maintenance. Tracking and managing operating expenses are crucial for maintaining the smooth functioning of the business and ensuring profitability.

Non-Operating Expenses:

Non-operating consists of one-time or irregular costs that are not directly related to the core operations of the business. Examples of non-operating expenses include legal fees, restructuring costs, losses from asset sales, and interest expenses. While these expenses may not occur regularly, they still impact the overall financial performance of the business.

Capital Expenses:

Capital involves investments in long-term assets that provide future benefits to the business. This category includes expenditures on property, equipment, machinery, vehicles, and other fixed assets. Capital expenses are recorded as assets and depreciated over their useful life, rather than being expensed immediately like operating expenses.

Tax-Deductible Expenses:

Tax-deductible are those expenditures that businesses can deduct from their taxable income, thereby reducing their tax liability. These expenses typically include costs incurred in the ordinary course of business, such as rent, utilities, salaries, supplies, and certain business-related travel expenses. Understanding tax-deductible expenses is essential for optimizing tax planning and maximizing tax savings for businesses.

Tax Implications Of Expenses – Knowledge You Crave!

Understanding the tax implications of different types of expenses is crucial for businesses to optimize their tax planning and minimize their tax liabilities.

Certain expenses may be deductible for tax purposes, reducing the taxable income and ultimately lowering the amount of tax owed.

By identifying deductible expenses, businesses can maximize their tax savings and improve their overall financial performance.

Additionally, compliance with tax regulations is essential to avoid penalties and ensure accurate tax reporting. By properly categorizing expenses and maintaining detailed records, businesses can demonstrate transparency and accountability to tax authorities.

Consulting with tax professionals can also provide valuable insights into tax-saving strategies and ensure compliance with ever-changing tax laws.

Overall, understanding the tax implications of expenses is vital for businesses to effectively manage their tax obligations and maximize their financial efficiency.

What Is Not Considered An Expense Account – Discover It!

Not everything that involves financial transactions qualifies as an expense account. While expense accounts track the money spent on various operational activities, certain items are not considered expenses within the accounting framework.

One significant distinction is between expenses and assets. Unlike expenses, which represent costs incurred to generate revenue, assets are resources owned by the company that provide future economic benefits.

Assets comprise tangible entities such as property, equipment, and inventory, alongside intangible resources like patents and trademarks.

Additionally, liabilities are another category of financial items that are distinct from expenses. Liabilities represent obligations owed by the business to external parties, such as loans, accounts payable, and accrued expenses.

While expenses reflect outgoing funds related to day-to-day operations, liabilities represent debts or obligations that the business has incurred but has not yet paid.

Understanding the difference between expenses, assets, and liabilities is essential for accurate financial reporting and effective management of resources.

Common Misconceptions About Expense Account – Uncover The Truth!

Common misconceptions about expense accounts can often lead to confusion and misinterpretation in financial management.

One prevalent misunderstanding is the assumption that all financial transactions automatically qualify as expenses.

However, it’s essential to recognize that expenses represent specific types of expenditures incurred in the process of generating revenue, such as operational costs.

Additionally, not all expenses directly result in losses; many are necessary investments that contribute to the growth and sustainability of the business.

Another misconception is the confusion between expenses and losses. While expenses can impact profitability by reducing revenue, they are essential components of conducting business operations.

On the other hand, losses typically refer to negative financial outcomes that result from various factors, such as market downturns or poor business decisions.

By understanding the distinction between expenses and losses, businesses can better manage their finances, allocate resources effectively, and make informed strategic decisions to drive long-term success.

Clarifying these misconceptions is crucial for maintaining accurate financial records and optimizing financial performance.

How To Identify Expense Accounts – You Must Know!

Identifying expense accounts requires a systematic approach and a thorough understanding of accounting principles. One effective method is to review the company’s financial transactions and categorize them based on their nature and purpose.

Analyzing expense receipts, invoices, and payment records can help identify common types of expenditures, such as utilities, rent, salaries, and office supplies.

Additionally, consulting with accounting professionals or utilizing accounting software can streamline the process by providing standardized categories for different types of expenses.

Furthermore, understanding the structure of financial statements, such as the income statement and balance sheet, can aid in identifying expense accounts.

Expenses are typically recorded on the income statement, where they are subtracted from revenues to calculate net income.

By examining the income statement, businesses can pinpoint various expense categories and assess their impact on overall profitability.

Additionally, expense accounts may also be reflected on the balance sheet, particularly in the form of prepaid expenses or accrued liabilities.

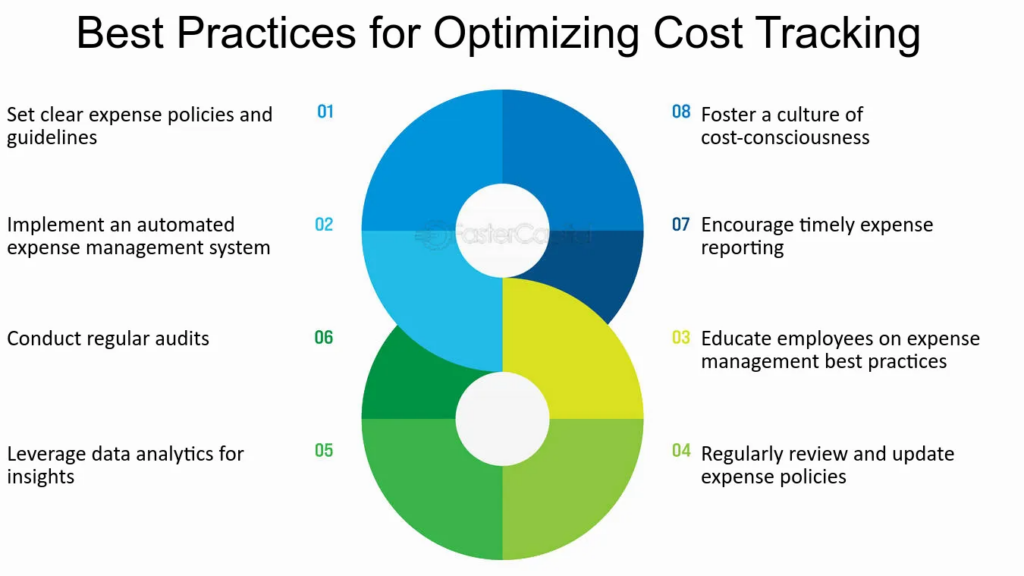

Best Practices For Expense Management – Check It Out!

Implementing best practices for expense management is crucial for businesses. Clear policies and procedures should be established to govern expense reimbursement and approval workflows.

Regular monitoring of expenses, aided by technology, helps identify trends and anomalies, facilitating timely corrective actions.

Periodic audits ensure compliance and identify areas for improvement, ultimately enabling businesses to control costs and achieve financial goals.

By fostering a culture of accountability and transparency regarding expenses, businesses can ensure adherence to established policies and procedures.

Moreover, providing training and support to employees on expense management practices enhances compliance and efficiency. Ultimately, effective expense management practices contribute to overall financial stability and growth for businesses.

Importance Of Budgeting And Forecasting In Expense Accounts – All You Need!

Expense accounts are crucial for budgeting and forecasting, providing insights into spending patterns and helping predict future expenses. By tracking expenses, businesses can create realistic budgets and make informed decisions to achieve financial goals.

Additionally, expense accounts to aid in strategic decision-making by identifying cost-saving opportunities and optimizing resource allocation.

Furthermore, expense accounts enable businesses to monitor their financial performance closely and identify areas where adjustments may be necessary.

By regularly reviewing expense data, companies can ensure that their budgets remain on track and make timely adjustments to their spending strategies.

Additionally, expense accounts serve as a valuable tool for evaluating the effectiveness of cost-saving initiatives and identifying areas for further improvement.

Overall, expense accounts are essential for maintaining financial discipline and driving sustainable growth in businesses.

Conclusion:

In short,

Expense accounts are vital for financial management, aiding in budgeting, forecasting, and tax planning, while implementing best practices ensures optimized resource allocation and improved financial efficiency.

With clear policies, regular monitoring, and a commitment to transparency, businesses can effectively control expenses and achieve their financial objectives, ultimately driving long-term success and growth.

FAQs

How can businesses track their expenses effectively?

Businesses can use accounting software to streamline expense tracking, maintain detailed records, and generate comprehensive expense reports.

What are the benefits of implementing expense management policies?

Implementing expense management policies enhances transparency, reduces the risk of errors or fraud, and promotes efficient resource utilization.

Why is it important to conduct periodic audits of expense accounts?

Periodic audits help ensure compliance with policies, identify potential discrepancies or inefficiencies, and improve overall expense management practices.